Approach

The financial world is built on tangibles—hard information such as economic data, price-to-earnings ratios, company news, and earnings. Events occur, and market participants react. This is where mass psychology comes into play, adding complexity to what would otherwise be a predictable formula.

Quantfury’s approach is based on three underlying market theories that govern the markets from social, mathematical, and economic perspectives. While markets can behave unpredictably, these principles generally hold true. Of course, there is no guarantee of success, but by embracing them, one may have a better chance of success than others.

Random Number Theory

Random number theory covers the world of mathematics and probability. It dates all the way back to 1863 and posits that stock prices follow no discernible trend. It stands to counter anyone who thinks they can outsmart the market with charts and technical analysis.

It’s important because anyone who regularly trades randomly will end up losing over the long run. Think of it like this: if someone were to trade repeatedly and randomly based on a flip of a coin, they’d win 50% of the time, and lose 50% of the time. However there’s a cost to flip the coin. Commissions, difference between bid and ask prices and various other fees will end up eating away from both sides of any trade, tilting the 50% win lose number exactly to the number that will encapsulate the cost of flipping the coin or making the actual trade.

Prospect Theory

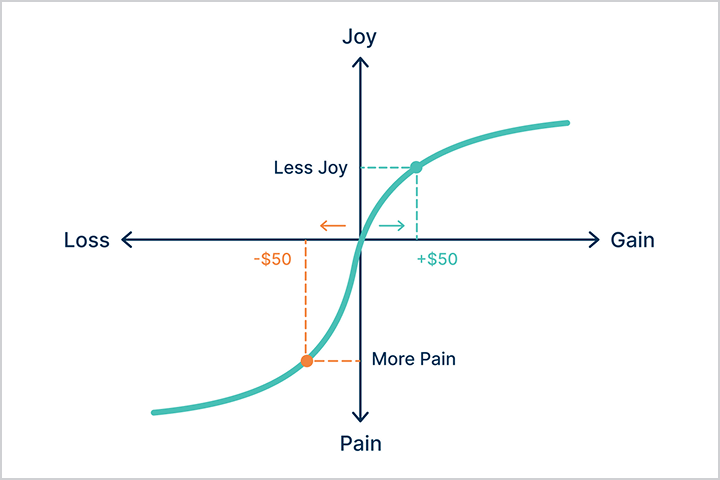

Human emotion and reactions to events introduce a layer of behavioral randomness to trading and investing. Prospect theory was developed first in 1979 by Israeli cognitive and mathematical psychologist Amos Tversky and Israeli-American psychologist Daniel Kahneman, who went on to win the 2002 Nobel Prize in Economic Sciences. The theory spearheaded a simple realization that it feels worse to lose $100 than it does to gain it. People, in other words, are emotional actors instead of rational ones, and that leads to unreal expectations and unproportional reactions to events, often directly opposed to economic self-interest.

At scale, trader behavior can be observed at a collective level as explored by the concept of fictional science of psychohistory that was described by famed science fiction writer Isaac Asimov in his Foundation series.

Market Efficiency Theory

Market efficiency theory is largely attributed to the work of American economist Eugene Fama, who won the Nobel Prize in Economic Sciences in 2013. His central thesis is that stock prices incorporate all available information at any given moment, making it extremely difficult to consistently outperform the market.

In a world of instantaneous communication and strict rules against the disclosure of non-public data and insider trading, that all means it’s essentially impossible to “beat” or “time” the market. While there are a few famous investors like Warren Buffett who have, in the past, outperformed the market over longer periods of time, it’s unlikely that you’ll be able to do the same. Rules passed since Buffett first got his start in the 1950s—and advances in technology—have only made markets more transparent and efficient.